I'm all for a good ol' fashioned showdown. But when it comes to the cash ISA vs stocks and shares ISA duel, it shouldn't be a fight.

It's not an either-or situation.

You can hold a cash ISA and a stocks and shares ISA at the same time, and they don't even have to be with the same provider.

But even though you can have both doesn't necessarily mean you should. Depending on your individual circumstances and financial goals, one of the two ISAs might make more sense for you. It also could be the case that each ISA serves its own purpose and helps you work towards a number of different financial goals.

What is a stocks and shares ISA?

A stocks and shares ISA is sometimes called an investment ISA (or, individual savings account). That's because you use this ISA to make investments in a tax-efficient way.

In a stocks and shares ISA, your tax treatment is different. You won't pay personal income tax on dividends or interest - no matter your own income tax rate. You also won't pay capital gains tax if you have any gains from investments too.

As an investor, you've got a smorgasbord of investment options for what to put inside your stocks and shares ISA. You could start with some exchange-traded funds (ETFs), add in investment trusts, government bonds, corporate bonds and investment funds, maybe sprinkle in some stocks and even fold in real estate investment trusts (REITs) if you'd like. The investments you choose for your stocks and shares ISA are entirely up to you.

It's important not to put all your eggs in one basket when you choose what to invest in. Diversifying your investments will help you spread risk across multiple assets as opposed to relying on one, often a sensible strategy to hit your personal financial objectives.

Can you hold cash in a stocks and shares ISA?

You can still hold cash in a stocks and shares ISA too. Though, that's not the best home for it.

Here's a great article on why cash can be a drag on your performance in a portfolio of investments.

If you have cash savings in a stocks and shares ISA, it's probably sitting there waiting for a ride to its final destination. After all, a stocks and shares ISA is for making tax-efficient investments, so you're depositing money into that account with the intent of buying and selling shares.

Read more:

What is a stocks and shares ISA?

Subscribe to Honey, our market newsletter

Your pocket guide to ISAs

What’s a cash ISA?

A cash ISA is one type of savings account where you might consider depositing your savings if you don't want to invest them.

But the return on a cash ISA isn't great, and it's particularly low in the context of rising UK inflation. While a variable rate cash ISA might be better primed to take advantage of rising interest rates, those rates are still falling very short of an annual inflation rate of 10.7% as of November 2022.

That said, if you have a short time horizon (or you're not yet sure of what that horizon even is) with the main goal of preserving your capital, they could be right for you.

If you want that money to grow, then a stocks and shares ISA is probably more up your street. Though, as with anything when it comes to investing, there is always the potential downside of the value of your investments going down as well as up. Whenever you invest, your capital is at risk.

The main benefit of a cash ISA is that your savings will earn interest without having to pay tax. This is the main way it differs from a traditional savings account (or, a non-ISA savings account).

But many wouldn't actually pay tax on interest from a regular savings account to begin with, because of their Personal Savings Allowance (PSA).

With your PSA, depending on your Income Tax band, you might be eligible to earn £1,000 of interest without having to pay tax on it. But that tax allowance only applies to Basic rate income tax payers, and tax rules are subject to change and your own personal circumstances.

Given the Bank of England (BoE) was reporting interest rates at ‘historically low levels' last year, you would need to save a lot to earn enough interest to exceed the £1,000 limit for a basic taxpayer.

For instance, if you were earning 1% interest on your savings account, you would need to have a minimum balance of £100,000 deposited to earn £1,000 in savings interest.

The difference between a stocks and shares ISA and a cash ISA

Now that you've got a sense of how the two accounts differ, you may be humming and hawing over which to choose. Technically, you can actually have both a cash ISA and a stocks and shares ISA at the same time. You can even pay into both ISA accounts in the same tax year.

But each ISA serves a different purpose, and because your tax year contribution's maximum allowance is split across all of your ISAs, it's wise to prioritise a certain account according to your financial objectives.

The 2023/24 tax year starts on 6 April 2023 and ends on 5 April 2024. This tax year has a £20,000 ISA contribution limit. While the current year’s allowance for ISAs is no different from the previous tax year’s ISA allowance, the overall tax environment is changing next year in a big way.

The tax rules in the UK have started to look quite different.

Here in the UK, the annual allowances for dividend income and outright investment growth (capital gains) fell from April 2023 onwards. With both allowance limits being chopped in half, and then again in 2024, it means a lot of investors are paying tax on their investments for the first time.

If you haven’t thought about investing tax efficiently, then, it might be wise to at least work out if a tax-efficient account like a stocks and shares ISA or self-invested personal pension (SIPP) could help now more than ever.

Eligibility to invest into an ISA or SIPP and the value of tax savings both depend on personal circumstances and all tax rules may change.

2023/24 dividend and capital gains allowances

If you aren’t investing using a stocks and shares ISA or a longer-term tax-efficient account like a SIPP you could be forking out a load of extra tax come April.

Often, investors will opt for the cheapest investment account out there and on the surface that makes sense. Why pay more than you have to? But investing solely in a general investment account (GIA) because it has a lower headline cost than an ISA risks missing the whole point, tax.

Now, it may be that you’ve decided you’re unlikely to go above your personal investment tax allowances. In which case, it’s probably true that an ISA wouldn’t be as useful. But, given those allowances are coming down fast (see the chart above) it’s maybe worth revisiting those assumptions.

New UK dividend tax allowance from April 2023

Putting the changes to the dividend allowance into perspective, a basic rate taxpayer earning £2,000 in dividends in the 2022/23 tax year, and earning the same dividend income for the next two years, would suddenly have to pay £87.50 in 2023/24, then £131.25 in 2024/2025.

The rise in dividend tax is even more pronounced for higher rate taxpayers, who would pay £506.25 in 2024/25, and additional rate taxpayers, who’d owe £590.25.

That’s a big chunk of change for anyone, and let’s not forget it could be even bigger if your dividend payments grow, like we all hope they do.

New UK capital gains tax rates from April 2023

Dividend allowances aren’t the only limits that got the chop in the 2023/24 tax year. The amount we can earn from the growth of our assets and not pay UK tax each year (your capital gains tax allowance) also fell from £12,300. First, to £6,000, then to £3,000 next year.

Of course, if you don’t sell any assets it doesn’t matter all that much right now. But eventually we all want to hit the sell button and actually put that money to use. In terms of tax purposes, it’s at that point that we’ll potentially have to pay tax on any gains we’ve made.

The thing is, making all that hopeful growth tax efficient needs to start long before you actually sell up and move on. If you get to that stage, the last thing you want is to be kicking yourself just because you didn’t use the most tax-efficient account to begin with.

Get planning for lower allowances and higher tax rates

It’s even more important to lend a thought to the tax benefits when you consider the route most of us want to take is into the higher tax bands at some stage in our working lives. With that prospective rise in salary and tax rate comes a rise in dividend and capital gains tax rate too.

For example, going from being a basic rate taxpayer to being a higher rate taxpayer means potentially paying 33.75% instead of 8.75% on dividends above the allowance.

That’s even more of an issue for the UK’s highest earners from April 2023 as the additional rate income tax threshold came down from £150,000 to £125,140. Granted, this bunch might not get a whole lot of sympathy from the rest of the nation’s savers and investors.

Read more:

2023 ISA income investing

Dividends and your stocks and shares ISA

Choosing the right investment account: GIA or ISA?

But the fact remains that anyone tipping the scales above £125,140 suddenly found themselves in a 45% income tax band, a 39.35% dividend tax rate, 20% in capital gains tax and staring down the barrel of two successive reductions in investment tax allowances.

ISAs and annual limits

All of these hits to what investors can earn before tax kicks in mean it’s just got even more important that we make our money as tax efficient as possible. That might mean looking beyond what our current investment gains and dividend income look like, and planning for what could come down the line.

It’s a harsh reality that a lot of investors investing outside of an ISA will eventually have to stump up tax payments eventually, when they could have just used an ISA instead.

Potential favourable tax treatments aside, it's still really important you make sure an ISA is right for you though. It could be that you genuinely get nowhere near these allowances or tax thresholds and never plan to. But that’s often the thing with investing. Compounding small amounts and incremental contributions over the years can really build up the snowball effect that good investing is based on.

Should I save my cash or invest it?

Putting your cash in a cash ISA may seem like a safe way to protect your money. Though if you're looking to grow your savings and beat inflation, cash is unlikely to be the answer.

When you invest in stocks and shares, you're putting your money to work. This is why your long-term (and by that we mean at least a five-year period) investment return with a stocks and shares ISA could be higher than with a cash ISA.

So let's say you want to save some money but you plan to take it out in the next few months. In that case, it could make sense to keep the cash in a general savings account rather than a cash ISA, where your contributions would eat away at your total allowance. Its value is also unlikely to fluctuate in the same way any invested money in a stocks and shares ISA could.

The trade-off is normally that you have to accept a lower rate of interest on your savings in exchange for that low level of risk on cash, when compared to the S&P 500 for example.

What are returns like for a cash ISA?

If you invested in a cash ISA between October 2021 to 2022, your average total interest rate for the year would have been 0.54% [1].

Meanwhile, The Consumer Prices Index including owner occupiers' housing costs (CPIH) flew up by 9.3% in the 12 months to November 2022. So your cash in a cash ISA would have eroded in value, and would be worth less than it was at the start of the year. That would mean you'd earned no gains from cash investments.

The value of your money would likely be greater had you invested it. For instance, if you had invested in the S&P 500 for the five years to 18 December 2022, your cumulative return would have been 67.9%.

So even though 2022 certainly wasn’t the best year for the US stock market, the overall trend remains positive. With a negative 8.4% return on the S&P 500 this year, it's important to note that you can get back less than you invested when you buy stocks and shares too. But the big picture tells a different story. And when you zoom out to the long-term investing point of view that’s crucial to building sustainable returns, the average interest rate in a cash ISA has never come close to such a high return.

Past performance is not a reliable indicator of future returns.

FE, as at 18 Dec 2022. Basis: bid-bid in local currency terms with income reinvested.'

Are stocks and shares ISAs risky?

While your return is likely to be greater with a stocks and shares ISA over the long term, that also means the level of risk is greater too.

That’s because you’re investing in the stock market, which means your return could go down or up. There’s a risk that you lose all of the capital that you invest. This would be much less likely in the case of a cash ISA.

If your ISA provider went under, your ISA would be covered by the Financial Services Compensation Scheme (FSCS) up to a maximum value of £85,000. This is the case for both cash ISAs and stocks and shares ISAs too.

How to transfer a cash ISA to stocks and shares ISA

The most important consideration when opening a stocks and shares ISA is whether it's the right decision for you. There are a number of factors to consider when assessing this, including your own financial goals, time horizon and tolerance for risk.

If you then decide you'd like to take the cash out of your cash ISA and invest it in your stocks and shares ISA instead, then it's entirely possible and relatively easy to do.

That's good news, because when you transfer money between your ISAs, you won't lose your allowance. But if you close one ISA and open another in a given tax year, your allowance won't reset. So whatever you may have deposited earlier on in the year cannot be re-added to your new ISA.

For more information on the ins and outs of the process, we've got you covered with our article all about ISA transfers.

Can I pay into a cash ISA and a stocks and shares ISA in the same year?

You sure can.

As long as you’re paying into different ISA types, you can pay into multiple accounts in the same tax year. And paying cash into both ISA accounts could be a good way to prepare for your short-term and long-term financial needs.

You could open a new ISA with a different provider every year if you wanted. You also don’t need to use the same provider for your cash ISA as you do for your stocks and shares ISA.

You can shop around if you’d like as well, you’re not married to any particular type of ISA nor to any particular provider.

If you do pay into a cash ISA and stocks and shares ISA in the same year, bear in mind your £20,000 allowance covers your contributions across both. So double-check that you’re not going over the limit.

Cash ISA or stocks and shares ISA?

To bring it right back around to where we started, cash ISAs and stocks and shares ISAs both have their place.

You could keep the money that you want to save and access in the short term in a cash ISA. But if you’re ready to take some investment risk and want to grow that money (and hopefully combat the effects of inflation) in a tax-efficient way, then a stocks and shares ISA might be better suited for your needs.

That’s because, unless the interest rate you receive on your cash ISA is higher than the rate of inflation, your money will be worth less in the future.

How will inflation impact my savings?

Let your mind wander to the chocolate aisle of your local Sainsbury’s for a moment. Picture a freshly-stocked shelf filled with Mars bars staring you in the eye.

In 1980, one bar would have cost you 15p. Today, the chocolatey goodness would run you 65p on average.

Inflation, or the rising cost of goods, is constantly eroding the value of what we can actually buy in the real world. All these years later you might still physically have the 15p in your hand but that Mars bar is now out of reach. Nightmare.

Alternatively, if it was 1980 and instead of buying the Mars bar you decided to take the 15p and deposit it in a savings account, you would need an average annual interest rate of around 2.9% to be able to afford that same Mars bar in 2022.

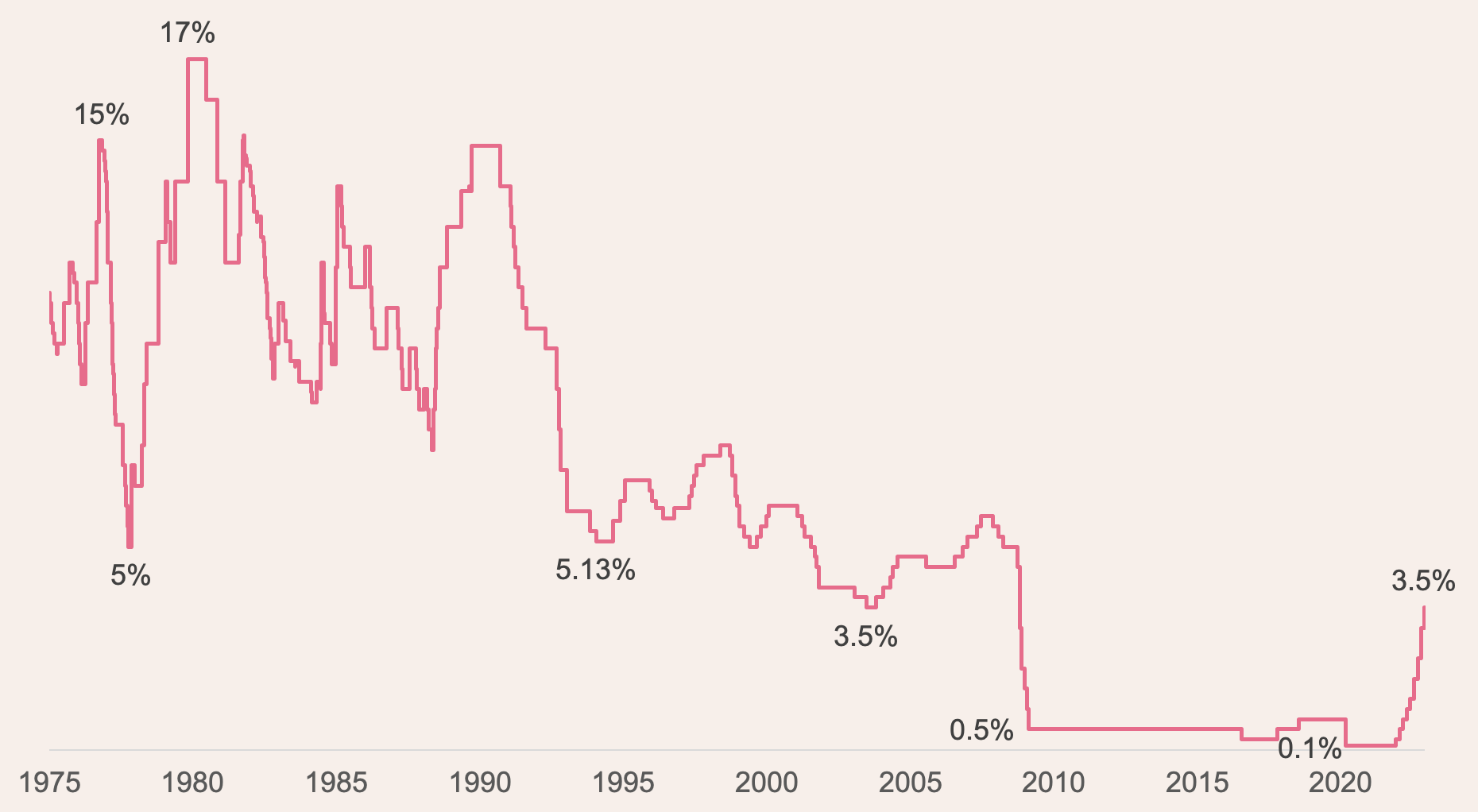

The Council of the Buildings Societies Association (BSA) reported the average interest rate for savings accounts was 10.3% in 1980. For the 12 months to November, the Bank of England reported the average interest rate for a one-year fixed rate ISA in the UK was 0.55%.

So these savings rates have fluctuated heavily over the years, and can’t necessarily be counted on to rise with inflation.

Interest rates have been very low since the global financial crisis in 2008 and, while they are rising in the US and UK, they aren’t covering inflation right now.

How can I open an ISA?

If you do decide to open an ISA, remember that the deadline is midnight on the 5th April 2023 for cash ISAs and stocks and shares ISAs. If you don’t open your ISA by then, you won’t be able to take advantage of this year’s £20,000 ISA allowance.

This is important to keep in mind because you can’t carry forward any unused ISA allowances. If you don’t use it, you’ll lose it.

If you do open an investment ISA, your investments can go down as well as up in value. If you’re comfortable with this risk and happy to choose your own investments, then a stocks and shares ISA might be right for you.

Our step-by-step guide on how to open a stocks and shares ISA is ready to walk you through the process if so.

[1] Bank of England Database, https://www.bankofengland.co.uk/boeapps/database/fromshowcolumns.asp?Travel=NIxAZxSUx&FromSeries=1&ToSeries=50&DAT=RNG&FD=1&FM=Jan&FY=2021&TD=31&TM=Dec&TY=2025&FNY=Y&CSVF=TT&html.x=66&html.y=26&SeriesCodes=LPMB6F2&UsingCodes=Y&Filter=N&title=LPMB6F2&VPD=Y.

Download the Freetrade investment app and join over 1 million UK retail investors that trust us already. See the most popular investments with a breakdown of the most traded stocks and most popular ETFs on Freetrade. Follow the IPO calendar and keep an eye on exciting new investment opportunities.

Important Information

SIPPs are a pension product designed for people who want to make their own investment decisions. You can normally only access the money from age 55 (set to rise to 57 from 6 April 2028). This article is based on current rules, which can change, and tax relief depends on your personal circumstances.

When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest.

Before transferring a pension you should ensure you will not lose valuable guarantees or incur excessive transfer penalties. Pensions are usually transferred as cash so you will be out of the market for a period.

Freetrade does not currently offer drawdown products for our SIPP.

The fees described in this article do not include any fees which may be charged by product manufacturers (e.g. ETF management fees).

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. If you are unsure whether our SIPP product is right for you, you should contact a qualified financial advisor.

Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).