When it comes to retirement planning, we’re short on time right from the start.

Mad, isn’t it?

It can feel like such a long time away but setting up a pension really needs to happen as soon as you’re earning, if you want a decent retirement lifestyle.

The good thing is that young people are aware of the need to contribute to their company pension or self-invested personal pension (SIPP) more than they’re given credit for.

The less good thing is they don’t always know the ins and outs of how to actually do it.

So, with no time to waste, let’s get stuck into the ways to go about saving and investing for your retirement in your 20s and 30s.

These are the sections we’ll look at:

- Reasons to start saving for your pension early

- Understand your pension contributions

- How much will I need to retire?

- How much should I contribute to my pension in my 20s and 30s?

- What investments should I put in my pension?

- Tips on saving to retire earlier

- Should I transfer my pension?

Reasons to start saving for your pension early

Older generations often have the benefit of gold-plated salary-for-life pensions to rely on.

If you’re in your 20s or 30s, you probably don’t. Or even if you do, they’re likely to be a lot less generous than they used to be.

That’s because firms realised how expensive these defined benefit pension arrangements ended up being and phased them out.

Instead, the onus is on us to save for our future selves, through defined contribution schemes.

How much we contribute to our pensions now and what we do with our money once it’s in there will have a direct impact on what lifestyle we’re able to give ourselves in retirement.

So kick-starting your retirement savings early is important.

But it’s not just about shoving as much cash under the mattress as possible.

Regardless of which account you use (ISA or SIPP), the main reason it’s so critical to start early is that the biggest asset you can give to your investments is time.

When you gain interest on your savings or investments, over time that interest gains its own interest and creates a snowball effect that gathers pace the longer you leave it.

Time really is money

There’s also really no substitute for time either. Unfortunately too many people find that out when it’s too late.

If we take the example of two pension savers, Sam and Alex, that all becomes even clearer.

Sam starts investing £100 at the end of each month when they are 25 until the age of 65.

The total amount they end up putting away over that period is £48,000. And if their investments were to achieve a 5% annual return they’d finish with a pot worth £141,768.

On the other hand, Alex begins later but doubles up on the pension contributions to try to make up for it.

They invest £200 at the end of each month from the age of 45, hitting the same £48,000 by 65.

But even with the same 5% annual return on their investments they end up with £77,611.

That’s over £64,000 less than Sam.

(If you want to play around the numbers and put in a few illustrations of your own, have a go here.)

Now, simply saying that saving as much as you can, as early as you can, and as often as you can is trite by any standard.

And our unique lives mean our ability to put money away may differ entirely from those around us, and can change throughout our lives just as much.

But as a simple illustration this serves to show the value time can add to your pension savings.

Whether it’s accumulating dividends, interest or just giving the stocks and shares in your portfolio time to grow, this compound interest lies at the very heart of long-term investing.

And for most of us, it doesn’t get more long-term than our retirement pot.

Better healthcare and longer life expectancies mean we are likely to spend much more of our lives in retirement.

We need to be actively involved in planning for that now, if we’re going to be comfortable later on.

What about if you are self-employed? See what your options are with our guide to self-employed pensions.

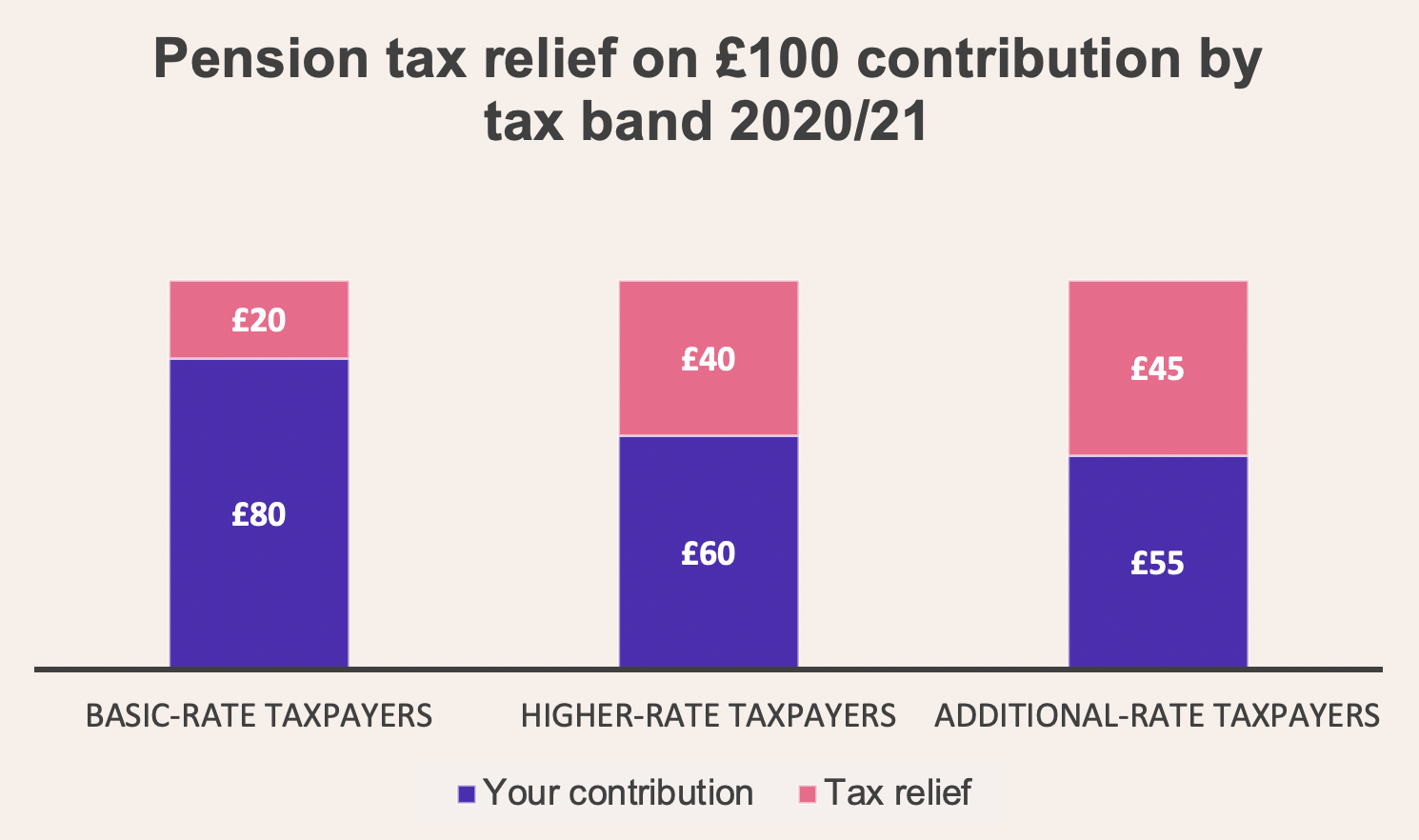

Tax relief

Thankfully we do still get a helping hand along the way from the government in the form of pension tax relief.

How much of your money is eligible for tax relief depends on how much tax you pay.

- If you’re in the basic-rate tax band and pay 20% tax on your earnings, you’ll receive 20% tax relief. That means a pension contribution of £100 from your salary into your retirement savings only costs you £80, with the government adding the remaining £20.

If you pay tax at a rate higher than the basic rate of 20% you can get even more tax relief on your contribution paid directly to you via your tax return.

- For higher-rate taxpayers paying income tax at 40%, this £80 contribution is boosted to £100 by basic rate tax relief being added to your pension. You can claim a further £20 back via your tax return. Therefore the £100 going into your pension will end up only costing you £60.

- And along similar lines, additional-rate taxpayers only have to contribute £55 to end up with a £100 contribution, as they can claim 45% pension tax relief, in line with their tax band.

Remember, the tax relief you are eligible for is judged by the highest level of income tax you pay.

These rules apply to tax relief in England and they can differ throughout the UK. You can find more on these figures as well as the details for Northern Ireland, Wales and Scotland online.

Understand your pension contributions

If you’re here to find out how to contribute to your pension you might be surprised - you’re probably doing it already.

Workplace pension & auto enrolment

If you earn more than £10,000 (from one job) and are aged between 22 and the state pension age, both you and your employer have to pay a percentage of your salary into a workplace pension scheme.

Since April 2019 the minimum contribution your employer must make is 3% of your salary.

And the minimum total contribution (you + your employer) is 8%. So, if your employer is putting in that 3% (they can pay more if they want to) your minimum contribution must be 5%.

Another point here is that your contributions are made from your pre-tax salary so, for most people, the hit to your spending power ends up being less than you think.

And finally there’s how these contributions are worked out.

For the current tax year, they are based on your ‘qualifying earnings’ which is all pre-tax employment income between £6,240 and £50,000.

So 8% of all of your earnings in this bracket will be automatically contributed to your workplace pension.

Government / state pension

You can also factor the state pension into your retirement planning. It’s a regular payment most people are entitled to, once they reach a certain age.

You can find out your state pension age here but if you’re currently aged between 20 and 39 it’s likely to be 68.

The amount you’ll get under the state pension also depends on how many ‘qualifying’ years of national insurance contributions you have under your belt by then.

You can find out what you’ve paid so far here.

At the moment the most you can expect from the full new state pension is £175.20 per week.

That’s not a king’s ransom by any means, and all the more reason to level-up your own contributions to kick start that compounding effect now.

How much will I need to retire?

It’s the question, isn’t it?

You’ll sometimes see general rules of thumb that say you need somewhere in the region of seven to ten times your income at the point of retirement or a certain amount by each stage in your life.

But before we look at that, putting a round number on it risks missing two important considerations:

When you want to retire and how you plan to live during retirement.

Younger people in particular will see changes to what they might want from retirement and what they can realistically plan for throughout their lives.

That’s because they are still likely to have a lot of life’s key expenditures ahead of them which will constantly change perceptions of value and will steadily refine what they deem to be achievable or even desirable standards of retirement living.

House deposits, weddings, children and all the life goals that often require money before we get to retirement ages will have a knock on effect here.

And that’s not even taking into account our salary trajectories, which can change massively over the years.

But we should take into account that, by and large, by the time retirement comes we’re likely to have fewer or lower expenditures than during our working lives.

A lot of people use their 25% tax-free cash from their pension upon retirement to help pay off their mortgage for example.

And by then the likes of childcare and the daily commute will probably be a thing of the past too.

With housing payments, often the biggest single expense, out of the way, this tends to mean we only need around half to two thirds of our final salary to achieve a similar standard of living as pre-retirement.

Whatever you decide later in life though, it’s important to remember that it’s easier to make changes to what you want at that stage rather than this one. You won’t be able to go back in time and save more.

How much should I contribute to my pension in my 20s and 30s?

With all of the above said, it’s still useful to have a ballpark figure in mind, to serve as a frame of reference if nothing else.

Let’s take someone earning the UK average salary for 2020 (around £31,000 according to Statista) and aiming to retire at state pension age on between half and two thirds of that (let’s say £19,000).

Take off the £9,110 from the state pension and, assuming a 30-year retirement, the remaining pension savings would need to provide an income of about £10,000 per year.

If our 30 year-old used a common rule of thumb and started to put a percentage of their salary equal to half their age (15%) away each month that would be £387.50, or £4,650 annually.

Now, that might seem a lot but remember - that takes into account tax relief and your employer contribution too. Like we said, it doesn’t have to break the bank, as long as you start early.

If our savvy saver kept up the monthly contributions until state pension age - currently 68 for them - then that £19,000 looks to be within reach. Try the maths out for yourself here.

Of course there are a lot of variables involved here, and we’ve assumed a 5% annual return on these pension investments which isn’t unreasonable but is likely to change from year to year.

And you might even look at that retirement age and think there’s no way you could wait that long.

Similarly, you might see your third age as a chance to just slow down or take on the projects you want in work, as opposed to stopping completely.

You can adjust the figures to help suit your goals and, just as importantly, help you realise just what sort of action you need to take now in order to meet them later on.

What investments should I put in my pension?

Just like we’ve said everyone has their own unique ability to contribute to and manage their pension, your personal investments are just that - personal.

And while we can talk in general terms about assets, you’ll have to decide what’s right for you.

For a lot of people, reading around and doing a bit of investment research will give them the confidence to go ahead. Getting to grips with the basics of investing can help.

But if that doesn’t sound like you, think about talking to a financial adviser instead.

That said, let’s talk investing.

Standard workplace pensions tend to change the asset mix in your retirement savings throughout your life for you.

Most of the time they use your age as an indicator of how much risk to take, adding more when you’re younger, and decreasing it as you get close to needing the money.

The theory is that you have time on your side when you’re just starting your career and can afford for higher risk assets in your portfolio to have a bumpier ride now, in the pursuit of higher returns.

As you get closer to retirement, the other part of the theory is that you don’t want to be taking too many chances - what if those riskier assets go through a volatile patch when you want to actually start using your money?

That’s why the see-saw often shifts from a share-heavy portfolio when you’re young, to fixed income-heavy assets like bonds later on.

Pension investments in your 20s and 30s

If you stand back from a historical stock market graph suddenly the short-term jagged edges disappear and you can see the general trend, which history shows us is towards the top right of the page.

Following this logic, that’s why it can make sense to be big on equities (company shares) when you’re young, leaving room for some bonds, commodities like gold and even property to provide diversification.

But while having your full working life ahead of you can make equities attractive at the start, it’s incredibly difficult to predict the winners and losers 35 years out.

Look at the developments of the past 35 years - the companies that have benefited, the countries facilitating new trends and the sectors moving the needle.

That’s why diversification by geography, sector and company size is key too.

While the general idea here is to give your investments as much opportunity to tap into as many sources of growth as possible, ultimately it has to suit your tolerance for risk.

Creating a portfolio with a diverse set of assets in line with your goals and risk tolerance means you’re open to opportunities without being overexposed to a single company or theme.

One example is having broad exchange-traded funds (ETFs) covering global markets form the bedrock of your equity exposure.

You can supplement these holdings with smaller positions in individual companies or assets like investment trusts in what is called a ‘core and satellite’ approach.

Tips on saving to retire earlier

Some employers will offer to contribute more to your pension if you do too. It’s worth asking about what their position is, and taking full advantage of any perks here if you can.

In your twenties and thirties it can feel like you’re constantly paying for things that don’t immediately show their worth, like insurance or new tyres for the car.

You can start to resent payments like these but remember - this is your retirement you’re saving for and will hopefully eventually benefit from.

Make sure you’re saving regularly too. It breaks up what can feel like a mammoth task into achievable chunks.

And when you invest at regular intervals, say monthly, you’ll naturally catch both the highs and lows of the market.

The result is that, over the long term, you tend to achieve a return somewhere in between, without trying to guess when the best time to invest is.

Time in the market is better than timing the market.

But if you are truly set on retiring earlier then consider upping your pension contributions.

In general most people can contribute tax efficiently up to the lesser of annual earnings and £40,000 each tax year.

However, beware if you are a high earner making more than £200,000, as the £40,000 allowance may be reduced to as little as £4,000.

Should I transfer my pension?

Young people today are predicted to change jobs up to 14 times during their careers. That means it will become very easy to lose track of a pension pot or two.

According to the Association of British Insurers around £19.4bn is currently sitting in lost or unclaimed pensions in the UK.

Don’t become part of this statistic.

The ease of keeping all your pensions in one place might be a reason to consider transferring them into a SIPP.

Other reasons might be that your current provider(s) have pension fees, limited investment options or poor visibility of what you’re actually invested in.

But don’t rush into it.

Before you make any changes to your current pension plans, you need to make sure transferring would be right for you. If you need to, get help from a financial adviser.

Here are some things to think over:

- Is your current provider going to charge you any exit-fees?

- Will any market value adjustment (MVA) apply on transfer from your existing provider?

- Will you lose any valuable benefits or guarantees?

- Consider how long the transfer might take and what impact this might have on your existing portfolio.

At Freetrade, we think investing should be open to everyone. It shouldn’t be complicated, and it shouldn’t cost the earth. Our stock trading app makes it simple for both beginners and experienced investors. And costs are low. You can buy and sell shares commission-free and take advantage of fractional shares (buy just a part of a share).